.jpg)

The Delaware coastline remains one of the Mid-Atlantic’s most compelling regions for secondary home ownership and real estate investment. Characterized by its logistical accessibility—offering streamlined transit corridors from major metropolitan hubs including New York/New Jersey, Philadelphia, Baltimore, and Washington, D.C.—the region boasts a highly favorable property tax structure relative to neighboring states.

This comprehensive guide serves as a strategic overview for prospective buyers seeking to navigate the nuances of the Delaware coastal market. It outlines property acquisition protocols, localized financing options, risk mitigation strategies, and asset management considerations.

(Note: For real-time, MLS-verified data and localized market analytics, please consult with The Real McCoy Group ... www.therealmccoygroup.com.)

Delaware Coastal Market Overview

The real estate ecosystem along the Delaware shore exhibits pronounced seasonal dynamics, with transaction velocity and demand peaking during the late spring and summer quarters. Asset valuations fluctuate considerably based on property classification—ranging from low-maintenance condominium units to expansive multi-family oceanfront estates—and proximity to primary beach access.

It’s a fast-moving market, especially during the peak spring and summer touring months when inventory tightens up fast. At the same time, high demand for short-term rentals means properties in highly walkable areas close to local shops and restaurants pull in a serious premium. Want to check out the latest median sales prices, average days on market, or current trends? Just shoot us a message to get the newest Coastal Market Performance Report from The Real McCoy Group.

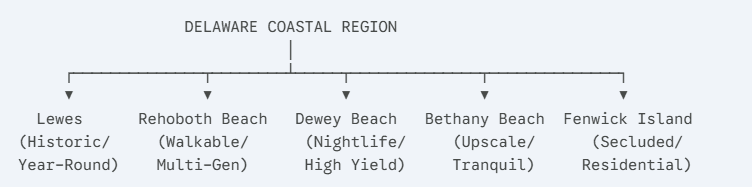

Municipal Profiles & Investment Jurisdictions

Rehoboth Beach — Premier Multi-Generational Walkability

- Strategic Value Proposition: Anchored by an iconic boardwalk, award-winning culinary establishments, and robust commercial infrastructure, this municipality commands some of the highest gross rental yields in the region.

- Target Buyer Profile: Capital-preservation buyers and institutional or private investors prioritizing high-occupancy seasonal rental income.

- Market Dynamics: Characterized by elevated price-per-square-foot valuations and consistent year-over-year capital appreciation, offset by intense market competition.

Bethany Beach — Exclusive Residential Tranquility

- Strategic Value Proposition: Distinguished by its low-density, family-oriented atmosphere, boutique commercial zones, and managed coastlines.

- Target Buyer Profile: Discerning buyers seeking a refined multi-generational retreat coupled with high retention rates among repeat seasonal tenants.

- Market Dynamics: Showcases strong price stability and low inventory turnover; the rental window is highly stable but more concentrated around peak summer months.

Dewey Beach — High-Yield Yield Optimization

- Strategic Value Proposition: Celebrated for its vibrant nightlife, coastal music venues, and comprehensive water sports infrastructure, situated optimally between the Atlantic Ocean and the Rehoboth Bay.

- Target Buyer Profile: Return-on-investment (ROI) driven investors targeting short-term weekend premiums and high-density occupancy models.

- Market Dynamics: Features high rental velocity; however, operations require rigorous property management oversight due to intensive tenant turnover.

Lewes — Historic Permanence & Year-Round Stability

- Strategic Value Proposition: As "The First Town in the First State," Lewes offers historic architecture, direct access to the Cape May-Lewes Ferry, and Cape Henlopen State Park, supported by a well-established, year-round civic infrastructure.

- Target Buyer Profile: Buyers looking for a secondary residence suitable for shoulder-season and off-season occupancy, or those planning an eventual transition to primary residency.

- Market Dynamics: Offers a highly stable market insulated from extreme seasonal valuation swings, though it yields lower high-volume weekly rental revenues than oceanfront options.

Fenwick Island — Secluded Coastal Privacy

- Strategic Value Proposition: Positioned at the southernmost border of the state, this municipality offers a quiet, predominantly low-density residential environment with minimal commercial encroachment.

- Target Buyer Profile: High-net-worth individuals prioritizing long-term asset appreciation, privacy, and dedicated family use.

- Market Dynamics: Characterized by limited inventory and steady demand from a niche demographic of multi-generational coastal residents.

Financing Mechanics for Secondary Coastal Assets

Securing debt equity for a coastal secondary residence requires navigating distinct underwriting criteria. Lenders evaluate these assets through specific risk frameworks:

- Conventional Secondary Home Mortgages: Tailored for buyers intending to occupy the property for a portion of the year without immediate commercial monetization. These instruments typically require a premier credit profile and down payments starting at 10% to 20%.

- Investment and Portfolio Loans: Required when the primary intent is to operate the asset as a short-term rental business. Underwriting focuses on the property's debt service coverage ratio (DSCR), often requiring larger cash reserves, 20% to 30% down payments, and adjusted interest rate structures.

- Cash Acquisitions: Capital deployment via cash remains a powerful tool in competitive coastal sub-markets, significantly accelerating closing timelines and enhancing offer strength.

Advisory Note: Early-stage pre-approval via financial institutions well-versed in coastal underwriting is imperative. The Real McCoy Group maintains a vetted network of regional lenders specializing in Delaware shore underwriting, structural cross-collateralization, and integrated flood insurance compliance.

Regulatory Compliance, Taxation, and Municipal Ordinances

Delaware presents an attractive tax environment, yet municipal and county variations require careful due diligence.

- Ad Valorem Tax (Property Tax): Delaware features substantially lower property tax assessments than neighboring Mid-Atlantic jurisdictions. However, exact rates are subject to specific county (Sussex County) and municipal assessments.

- Income and Lodging Tax Obligations: Gross rental income earned by out-of-state owners is subject to state tax reporting requirements. Furthermore, short-term rentals are subject to Delaware State lodging taxes, along with localized municipal accommodations taxes.

- Short-Term Rental (STR) Legislation: Regulatory frameworks vary significantly by town code and Homeowners Association (HOA) bylaws. Municipalities may impose strict rental licensing protocols, occupancy caps, parking mandates, and seasonal operational restrictions.

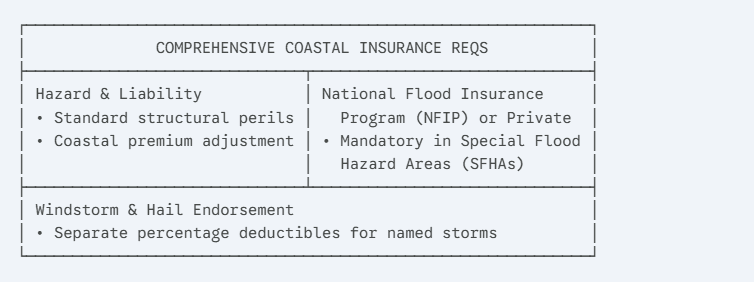

Risk Mitigation: Insurance and Coastal Engineering

Owning real estate in a dynamic coastal environment necessitates a sophisticated risk management strategy to protect your asset.

- Hazard and Liability Insurance: Standard homeowner policies require specialized underwriting adjustments to account for coastal proximity, with premiums reflecting geographic exposure.

- Flood Insurance Realities: Properties located within FEMA-designated Special Flood Hazard Areas (SFHAs) require dedicated flood policies via the National Flood Insurance Program (NFIP) or private syndicates. Incorporating these line-item premiums into cash-flow models is standard practice.

- Windstorm and Excess Topography Endorsements: Many underwriters implement separate, percentage-based deductibles for named tropical storms or hurricanes.

- Structural Engineering Upgrades: Capital improvements such as elevated pilings, impact-resistant storm shutters, and reinforced roofing systems reduce structural risk while generating premium credits with major insurance carriers

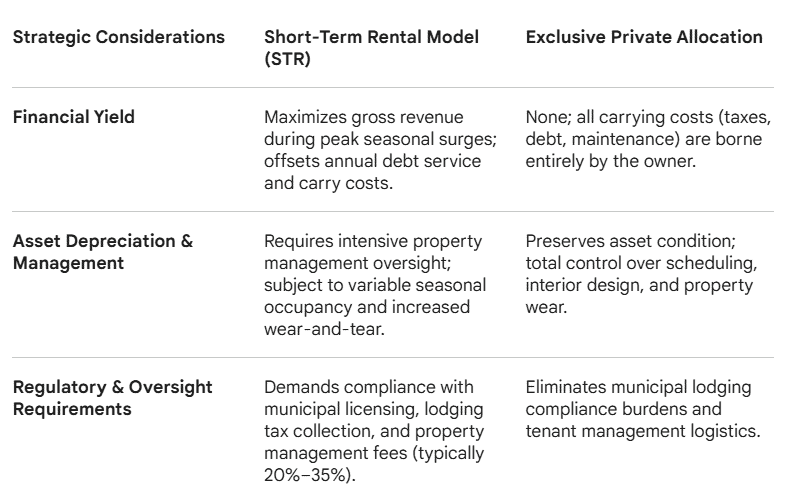

Illustrative Modeling of Annualized Occupancy Velocities

- Conservative Model: 25% to 40% annualized occupancy, heavily weighted toward shoulder and peak summer months. Ideal for owners prioritizing personal access while securing modest supplemental income.

- Optimized Investment Model: 60% to 80% occupancy within primary high-demand municipal corridors during peak operational periods. Optimized for maximum gross returns and structured cash flow.

The 10-Step Coastal Acquisition Protocol

- Geographic and Budgetary Scoping: Determine your target acquisition budget and identify preferred municipal jurisdictions based on your investment goals.

- Financial Qualification: Secure formal mortgage pre-approval with a specialized coastal lender to establish clear purchase parameters.

- Brokerage Engagement: Retain The Real McCoy Group as your dedicated buyer's representative to gain access to off-market inventory and local expertise.

- Targeted Property Sourcing: Conduct rigorous digital and physical property tours of curated listings matching your criteria.

- Regulatory and HOA Due Diligence: Review all relevant HOA regulations, restrictive covenants, zoning codes, and municipal short-term rental rules.

- Undergo Property Inspection: Order a comprehensive home inspection accompanied by a specialized coastal condition addendum to assess structural integrity.

- Analyze Insurance Costs: Secure a formal flood zone determination and obtain detailed premium quotes for hazard, wind, and flood insurance policies.

- Finalize Financing and Permitting: Complete the underwriting process while simultaneously filing for any required municipal occupancy or rental licenses.

- Title Examination and Conveyance: Execute a clear title search, bind all necessary insurance instruments, and finalize the closing process.

- Implement Asset Management: Establish relationships with local property managers, winterization contractors, and maintenance teams to secure the property.

Frequently Asked Questions

1. Is flood insurance federally mandated for all Delaware coastal properties?

If the property relies on conventional or institutional financing and sits within a FEMA-designated Special Flood Hazard Area (SFHA), flood insurance is legally mandated. Even outside these zones, carrying flood insurance is highly recommended for coastal assets.

2. Are out-of-state purchasers subject to acquisition restrictions in Delaware?

No. The State of Delaware maintains an open real estate market with no legal restrictions or alternative fee structures imposed on out-of-state or international buyers.

3. Are short-term rental models permitted across all Delaware shore locations?

No. Short-term rental allowances are subject to a patchwork of municipal codes, county zoning, and specific HOA covenants. A thorough review of these rules is required before purchasing a property.

4. What capital reserves are typically required for a secondary home down payment?

Conventional secondary home financing generally requires a minimum down payment of 10% to 20% for qualified buyers. Properties categorized as pure investment assets typically require 20% to 30% down.

5. What constitutes the peak rental period along the Delaware shoreline?

The primary rental season begins over Memorial Day weekend and runs through Labor Day weekend, with extended shoulder-season demand keeping properties active well into September and October.

6. How are property taxes calculated for Delaware vacation homes?

Delaware features some of the lowest effective property tax rates in the nation. However, the total tax bill is a combination of Sussex County taxes, school district assessments, and any applicable town-specific municipal taxes.

7. Is professional property management necessary for secondary coastal assets?

For owners who do not reside in the area or those using the property as a short-term rental, hiring a professional property manager is highly recommended. They handle emergency maintenance, winterization, guest relations, and local compliance.

8. How does structural elevation influence the long-term cost of ownership?

Elevation is a key factor in coastal risk assessment. Properties built above the base flood elevation (BFE) benefit from significantly lower flood insurance premiums, less structural risk during storms, and better long-term asset preservation.

Strategic Next Steps

To begin exploring the Delaware coastal real estate market with a trusted local advisor, contact The Real McCoy Group. Our team provides verified MLS market reports, comprehensive town-by-town valuation analytics, vetted lender and insurance networks, and tailored acquisition strategies designed around your financial goals.

Contact The Real McCoy Group today and schedule a private consultation.

Document Analysis Date: May 18, 2026. Data verification should be performed using current local MLS and Sussex County public registries prior to executing any binding legal contracts.

The information provided in this article is for educational and informational purposes only and does not constitute formal financial, legal, tax, or real estate investment advice. While we strive to ensure accuracy, coastal real estate markets, municipal ordinances, tax laws, and insurance regulations change frequently. All market figures, rental yields, and drive times are illustrative placeholders and should not be relied upon for investment decisions. Readers are strongly encouraged to consult with qualified legal, financial, and insurance professionals, as well as licensed real estate agents at The Real McCoy Group, to verify current local data and compliance requirements before executing any property acquisitions.

Social Links Header