.jpg)

Purchasing a coastal home—whether it is a primary residence, a seasonal vacation getaway, or a strategic investment property—is an exciting milestone. However, the coastal real estate landscape features unique variables, from shifting market dynamics and specialized loan structures to localized closing regulations and unique insurance requirements.

To maximize opportunities in today's market, buyers must understand current real estate trends, specialized financing structures, and the critical importance of robust preparation.

1. The Post-Pandemic Coastal Market: A Return to Normalcy

The coastal real estate market has transitioned away from the unprecedented frenzy of the pandemic era. During that peak, record-low interest rates and a massive surge in remote work drove extreme demand. Sellers frequently overpriced properties, skipped inspections, and routinely "leapfrogged" historical neighborhood valuations.

Today’s market operates under a much steadier, healthier cadence:

- Balanced Timelines: The bottlenecked logistics of the pandemic—where home inspections, appraisals, and underwriting faced massive delays—have resolved. Standard settlement timelines have returned to a predictable three to four weeks.

- Realistic Pricing and Negotiation: Price appreciation has leveled out, and values in certain segments have adjusted slightly due to higher interest rates. Sellers must price their properties strategically based on current market data, as buyers are successfully negotiating deals averaging 2% to 3% below asking price.

- The Return of Contingencies: Buyers once again possess the leverage to include critical protection in their offers, such as settlement assistance and home sale contingencies (provided the buyer's current home is already under contract).

While high-demand neighborhoods, entry-level price brackets, and premier waterfront properties can still trigger multiple-contract scenarios, the broader market now offers a more flexible environment for buyers.

2. Specialized Financing Options for Coastal Properties

Coastal real estate spans an array of property types, including luxury estates, single-family farmhouses, and high-density condominiums. Standard conventional loans are not always the best fit—or even viable—for these diverse structures. Navigating this requires understanding specialized lending programs.

Debt Service Coverage Ratio (DSCR) Loans

For investors looking to acquire beach property specifically for rental income, Debt Service Coverage Ratio (DSCR) loans provide an exceptional alternative to traditional financing.

Instead of evaluating personal tax returns, pay stubs, or historical employment data, a DSCR loan focuses entirely on the real estate asset itself. The lender evaluates the projected monthly rental income of the property against its total monthly carrying costs, including the mortgage principal, interest, property taxes, homeowner's insurance, and mandatory condo or homeowner association (HOA) fees. If the rental income covers or exceeds these operational expenses, the loan can be approved, bypassing the rigorous personal income verification required by conventional underwriting.

Jumbo and Non-Conforming Loans

When a property's purchase price exceeds the standard limits set by the Federal National Mortgage Association (Fannie Mae) and the Federal Home Loan Mortgage Corporation (Freddie Mac), buyers enter the realm of non-conforming Jumbo loans. The conforming loan boundary hovers in the low-to-mid $800,000s, varying dynamically by region.

Beyond funding high-end luxury properties, Jumbo lenders often offer niche products with flexible underwriting guidelines. For instance, self-employed buyers with sophisticated tax strategies can leverage alternative bank-statement programs through Jumbo investors rather than submitting traditional personal tax returns.

Capital Optimization Strategies

Even affluent buyers shopping in the luxury tiers frequently utilize financing rather than making all-cash offers. When capital markets deliver strong yields, keeping liquidity intact within investment portfolios and financing the home at prevailing market interest rates often makes superior financial sense.

It is important to note that secondary residences and investment properties generally demand higher down payments than primary homes. To preserve liquid cash reserves, buyers can strategically leverage alternative funding avenues, such as borrowing against a 401(k) account, to hit required down payment benchmarks.

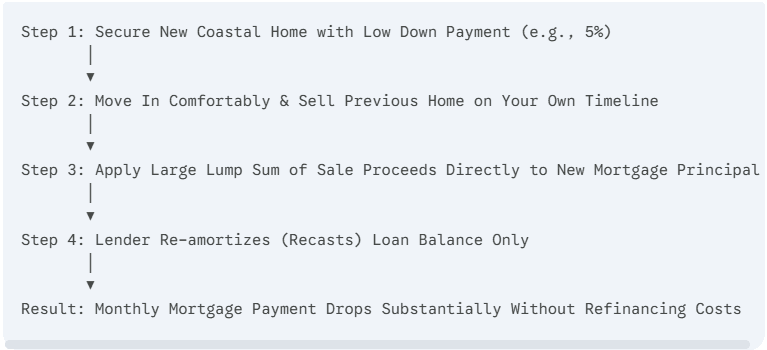

3. The Power of Financial Flexibility: The Loan Recast

A frequent challenge for buyers transitioning to a coastal community is timing the sale of their current home with the purchase of their new beach property. Attempting to coordinate simultaneous settlements on the exact same day injects immense stress into the moving process.

The loan recast serves as a highly effective mechanism to solve this logistical hurdle.

Under this strategy, a financially stable buyer purchases their new coastal home utilizing a standard loan with a lower down payment (e.g., 5%), leaving their retirement accounts and core investments untouched. This allows them to move into the new property at their own pace.

Once their previous home sells and they walk away with the net proceeds, they deliver a lump-sum payment directly to the new mortgage lender. Instead of altering the original interest rate or loan term, the lender simply re-amortizes the remaining, reduced principal balance. This instantly drops the monthly obligation—for instance, reducing a payment from $3,800 down to a highly manageable $1,200—without incurring the steep closing costs, legal fees, or administrative friction of a full refinance.

4. Why Local Underwriting Expertise is Non-Negotiable

Selecting a local lender rooted in the specific coastal market is paramount, particularly when buying a condominium. Condominium underwriting is highly complex. Lenders do not merely evaluate the borrower; they must thoroughly audit the complete financial health of the entire condominium association.

A local lender frequently maintains pre-approved portfolios of regional condo buildings. Conversely, an out-of-state lender entirely unfamiliar with local developments must initiate a lengthy discovery process from scratch. This includes issuing exhaustive condo questionnaires, scrutinizing capital reserve studies, checking for historical budget delinquencies, and analyzing complex master insurance policies. Working with a local specialist prevents transaction delays and shields the buyer from unforeseen liabilities.

5. Total Cost of Ownership and Coastal Compliance

When establishing a real estate budget, buyers must look past the core mortgage principal and interest to calculate the absolute total cost of ownership. Coastal properties carry distinct regional expenses that heavily impact monthly cash flow:

- High-Value Transfer Taxes: Closing expenses vary significantly by state. For instance, Delaware features a 4% real estate transfer tax, typically split equally (2% each) between the buyer and seller. This represents one of the highest transfer tax structures in the nation and requires substantial cash upfront at settlement.

- HOA and Condo Fees: Amenity-rich coastal communities often carry significant monthly or quarterly association dues to cover collective grounds maintenance, bulk utilities, and building upkeep.

- Flood Insurance Protocols: Waterfront access comes with strict geographic insurance mandates. Properties situated on canals, bayfronts, or oceanfront zones almost universally require specialized flood insurance policies. These premiums must be accurately quoted and factored into underwriting calculations early in the process.

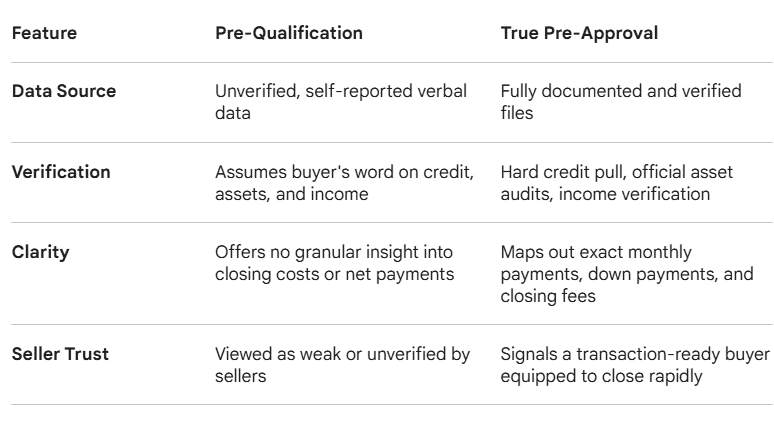

6. Pre-Qualification vs. True Pre-Approval

To position an offer competitively, buyers must understand the operational difference between a superficial pre-qualification and a verified pre-approval:

Completing a comprehensive pre-approval acts like packing for a trip the night before. Gathering complex legal documentation up front—such as active trust agreements, corporate tax structures, and state-compliant Powers of Attorney (POA)—eliminates panic later on. If a desirable property suddenly receives competing bids, a fully pre-approved buyer can instantly execute a firm, clean offer without scrambling for paperwork.

Conclusion

Securing a premium coastal home requires a blend of market awareness, strategic loan matching, and meticulous preparation. By partnering with hyper-local real estate and mortgage specialists, choosing the ideal financing program, and completing an upfront pre-approval, buyers can confidently navigate the process and turn their dream of coastal living into a secure reality.

Want to learn more?

Get the inside scoop on coastal financing. Watch the full episode here →

https://youtu.be/qJzbdbhAqQg

Social Links Header